As the COVID-19 virus continues to spread in the U.S., its impacts have reached every aspect of our lives and shook all sectors of the economy. Amid this crisis, there have been widespread worries that the disease could threaten the nation’s food production and supply systems and stoke inflation. Many began to wonder whether the food they need will continue to be available and affordable as we work our way out of the outbreak.

While we can’t track COVID-impacts on the agri-food sector in real time, I wanted to share some of the data currently available at USDA, which show that the U.S agricultural market will remain well supplied and food will continue to be affordable.

What we know is reassuring

The U.S. food sector is supplied by three sources; domestic production, imports, and what we have in storage. We also rely on a network of manufacturers and distributors to process agricultural outputs, prepare them for human consumption and move products from farms, to production facilities, and finally to consumers.

Currently, the outlook for domestic production of agricultural commodities, including cereals, meat and dairy is very good. We have sufficient quantities to not only feed our country but maintain robust exports even in the face of the COVID-19 pandemic. USDA’s World Agricultural Supply and Demand (WASDE) report for example, forecasts U.S. wheat production in 2019/2020 at 1,920 million bushels, up a little more than two percent from last year. The report also shows that current wheat supplies, particularly for bread wheats, are plentiful. U.S. wheat stocks are estimated at 970 million bushels, which is more than what we consume domestically for food in one year.

Data also show that we have adequate domestic supply of meat, eggs and dairy products to meet immediate demand. According to WASDE, red meat production for 2020 is forecast at about 56.7 billion pounds, up three percent from 2019, while production of poultry meat is forecast at 51.6 billion pounds, up almost three percent from 2019. Production of eggs and milk is also forecast higher in 2020 compared with last year. In addition, USDA’s most recent report on commodities in cold storage shows that at the end of February, total red meat in freezers was up 5 percent and chicken was up six percent from last year.

Another reassuring indicator is that the domestic supply chain has held up so far. Industries that are part of the food supply chain, such as meat packing operations and wheat and rice mills have been deemed as essential industry infrastructure and exempt from any shelter-in-place orders. And according to the Food Safety and Inspection Service (FSIS), the USDA agency responsible for regulating meat processors, closures of facilities regulated by the agency due to the disease outbreak have been limited, and temporary. Similarly, wheat and rice mills, which generally are not labor-intensive operations, have not had any significant disruptions.

Meanwhile, USDA continues to provide critical inspections and grading services including USDA quality grade marks—usually seen on beef, lamb, chicken, turkey, butter, and eggs— and audits for Good Agricultural Practices (GAP) and Good Handling Practices (GHP). In addition, to facilitate movement of fresh specialty crops to markets, the Department is focusing its Good Agricultural Practices audits on entities that are new to USDA audit verification program.

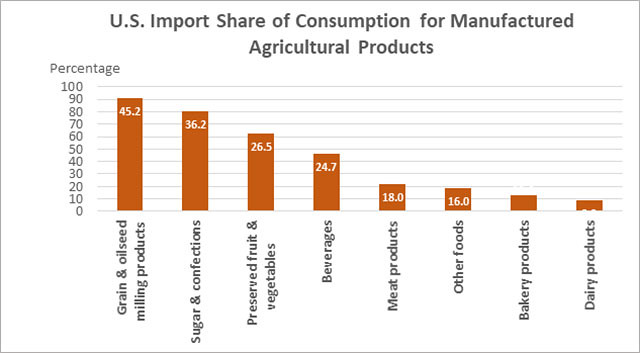

On the import side, the situation is less certain as we don’t have detailed data on conditions of our trading partners. Americans normally rely on food imports for about 15% of total food consumption. But for some products such as fruits and tree nuts (generally during winter months) and certain meat cuts, imports account for much higher shares. For those products, significant supply disruptions in source countries could potentially lead to shortages and higher prices in the U.S. market. However, industry and news reports on trade flows suggest that even countries heavily affected by COVID-19 spread, continue to ship food products and that there are no immediate risks of massive disruptions in the global supply chain.

So why do we see some empty shelves and higher prices?

At the beginning of the COVID-19 outbreak, as consumers rushed to stock up on essential food items, there was a sudden and large increase in demand for food products from grocery stores, which led to shortages and higher prices of some products. In addition, the dramatic reduction in restaurant traffic and food service demand (more than half of consumer food spending) led to an even greater increase in demand at the retail level. Producers and retailers typically plan for steady demand increases and were not prepared to deal with the rapid surge we saw with the onset of the crisis. But over the next few weeks, as retailors restock their shelves and demand from overstocked consumers decline, we will see fewer empty shelves and prices should stabilize or even decline. A good example is eggs, where increased demand from mid-March caused tight supplies and substantially higher wholesale egg prices; New York shell egg prices, reached a record $3.07 per dozen by the end of the month. But as retailers restocked their coolers, prices have begun to fall, and as of April 14, wholesale prices were down to $1.97 per dozen.

Another factor that will contribute to availability of food to consumers and likely put downward pressure on prices, is the drastic decline in demand from restaurants and hotels together with the surge in demand by food retailers. Womply (a private consulting firm) data on credit card transactions from local businesses nationwide show for example that restaurant sales on April 1 were about 50% lower than in the previous year (68% lower on March 21 compared with same time in the previous year). Meanwhile, grocery store sales were up 99% in the middle of March and 25% higher on April 1 compared with the same time last year. The shift in demand means that food that would have been sold to restaurants and hotels will be redirected, at least in part, to grocery stores and online food retailers. But these changes will take time and require operational adjustments along the supply chain. For example, meats supplied to restaurant and hotels are often cut and packaged differently than those sold in grocery stores. The same goes for dairy items typically sold to restaurants and food service, will need to be redirected and repackaged in the short-run for retail grocery sales. USDA has stepped in to help industries adapt. The egg industry, for example, is able to redistribute table eggs from foodservice warehouses to grocery stores to support the increase in consumer demand. The Department is also applying some labeling flexibilities to the Country of Origin Labeling (COOL) requirements to facilitate the re-distribution of food products from foodservice establishments to retail stores.

So overall, the supply and demand factors at play point to stable if not lower market prices in the next few weeks. April WASDE price forecasts were down from last month for most meats, eggs and milk and only slightly up for wheat and rice.

Sources of uncertainty

While the data and indicators we have are reassuring, we are dealing with an unprecedented crisis and there are many unknowns that could shape the situation in the next few weeks. For example, how the outbreak will evolve and whether it will cause significant labor shortages or logistical constraints will have an impact on food supply and prices in localized areas.

It’s also unclear how food consumption patterns will change as a result of the major shift to online shopping and ongoing restrictions on movement. According to the Food Industry Association (FMI), many shoppers have increased or are shopping online for the first time, as almost one-half of Americans have shopped online for grocery-type items in the month of March. This is more than twice the proportion of monthly online shoppers from FMI’s U.S. Grocery Shoppers Trends research one year ago.

Another key factor that will drive food availability and prices is how farmers and companies respond to changing market conditions. The U.S. agri-food sector is very agile and has shown time and again its ability to evolve quickly and innovate to respond to new situations.

Throughout this crisis, USDA’s Commodity Procurement Program remains fully operational and is working with Federal, state and local partners to purchase and distribute food to participants in domestic and international nutrition assistance programs. The Department is also working with vendors to extend as much contractual flexibilities as possible to continue to serve program recipients effectively during this time.

There are signs that the spread of the disease is slowing and we are hopeful that the worst is already behind us. But regardless of what the next few weeks or months might have in store for us, we do know that we have strong and resilient agricultural and food sector. Those farmers, food producers, and food suppliers will help continue the supply of safe, affordable, and healthy food for American consumers throughout the times to come.